Help Section

BETA - Content added daily

What would you like help with?

Enter a keyword or phrase

Matching Help Articles

tax-free cash, PCLS, UFPLS, lump sum, drawdown, Module 3, pension cash, tax-free lump sum, partial split

Set Up Tax-Free Cash in the App

Readphased retirement, step-down, reduced hours, career break, part-time, Module 4, Module 3, bridge income

Setting Up Phased Retirement

Readcare costs, later life care, residential care, Module 8, life events, resilience buffer, Module 5, stress test

Later-Life Care Planning

Readscenarios, named scenarios, save plan, load plan, My Data, Premium, compare plans, cloud sync, snapshot

Creating and Saving Scenarios

Readuser guide,user journey,Lifestyle Finance Calculator,module,25 year projection,getting started

From Vision to Reality: The Complete RetirePlan Journey

Readquiz,archetype,swipe,goals,blueprint , actions, vision, progress

How the Lifestyle Goal Planner Works

ReadBrowse the Article Library

Articles are presented latest first.

Select a category or leave blank for all articles

Select a category or leave blank for all articles

Search Box

Filter by Category: click to select

Passions & Pursuits

Passions & Pursuits

Passions & Pursuits

July 14, 2026

Cooling Your Home in a Warming Climate

UK summers are getting hotter, more uncomfortable, and even dangerous for older adults. Here is what you need to know about cooling your home effectively - and the options available at every budget.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

July 14, 2026

Releasing Equity from Your Home - Good Idea or Rip-Off?

Equity release is growing fast, and government and regulators are actively encouraging it. But the costs can be far higher than the headline suggests. Here is what to understand before anyone starts talking about your home.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

July 11, 2026

Can Your Pension Own Your Business Premises? SIPPs, SSAS and Commercial Property Explained

A SIPP or SSAS can buy the premises your business trades from, turning rent into a pension contribution. Here's how it actually works, and what's changing from April 2027.

Read MoreLifestyle Planning

Lifestyle Planning

Lifestyle Planning

July 11, 2026

RetirePlan UK: Your Lifestyle-first Planning Companion

.jpg)

Most retirement planning starts in the wrong place. RetirePlan's lifestyle-first approach turns that around - here's how starting with your dreams creates a better plan and a better life.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

July 3, 2026

Pensions and Inheritance Tax - What now?

From April 2027, unused pension funds count towards your estate for inheritance tax. The old ISA-first, pension-last strategy no longer holds - here is what changes and what to think about now.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

July 2, 2026

April 2027 ISA changes

From April 2027, significant ISA rule changes will affect how much cash you can hold in a Cash ISA and how interest is taxed across ISA types. Here's what you need to know.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

July 2, 2026

Pensions v ISA’s – which is best?

.jpg)

Pensions and ISAs are two of the most powerful savings tools available to UK savers - but the rules are changing on both fronts. Here's what you need to know to make the most of each in the years ahead.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

July 2, 2026

UK Gifting - tax rules and optimisation tips

With inheritance tax rules changing significantly by 2027, gifting during your lifetime has never mattered more. Here's how the rules work, what allowances are available, and the crucial traps to avoid - including the rules on gifting your home.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

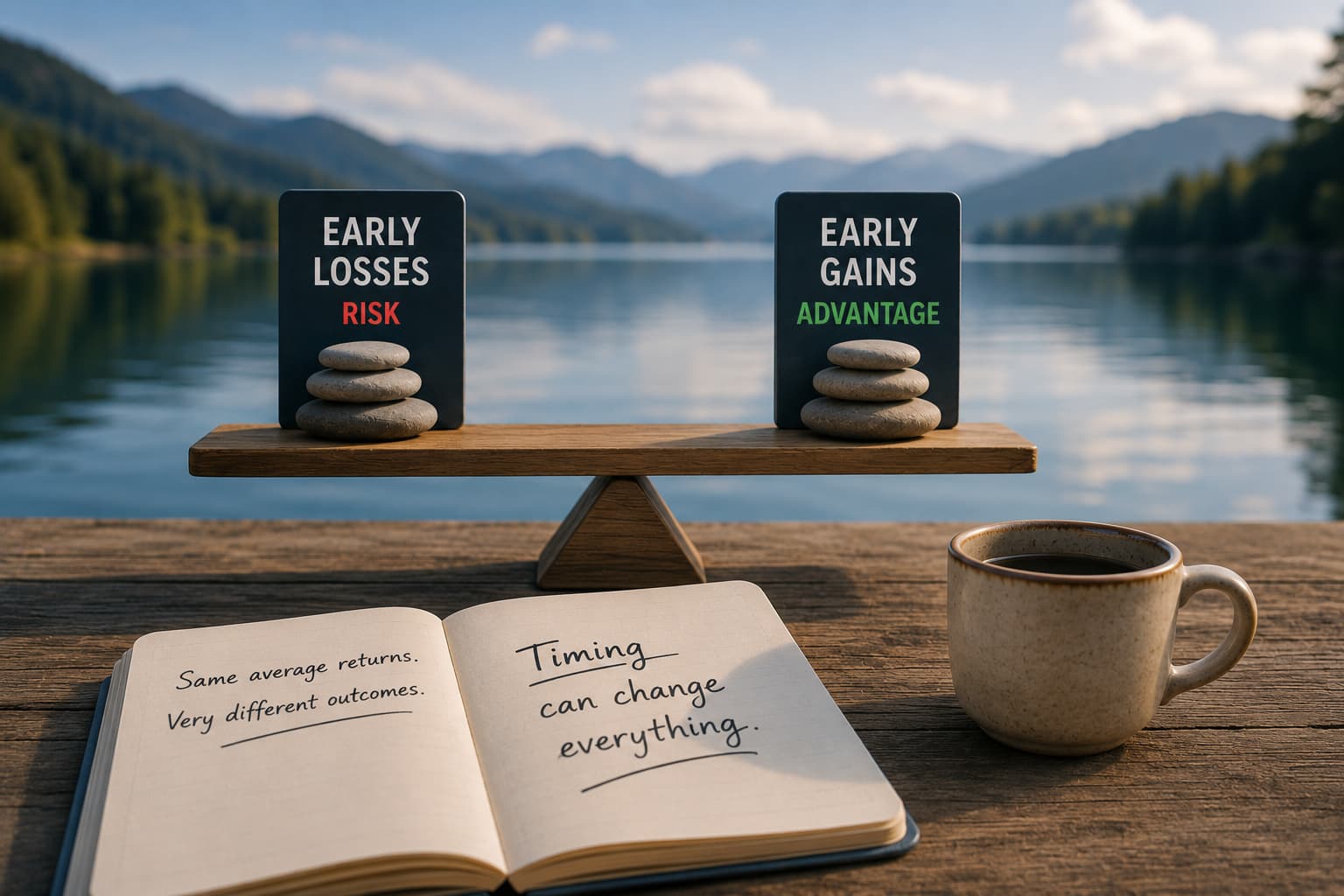

July 1, 2026

Sequence of Returns Risk

Two people. Same average investment returns. Completely different retirement outcomes. Understanding sequence of returns risk could be one of the most important things you do before starting drawdown.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

June 13, 2026

The Pensions Wake-Up Call: Why "I'll Sort It Later" Is the Most Expensive Plan of All

.png)

A new government commission warns that 15 million working-age people are undersaving for retirement. Here's what the findings mean, and why the earlier you act, the easier it gets.

Read MoreLifestyle Planning

Lifestyle Planning

Lifestyle Planning

June 3, 2026

Achieving Your Goals

This article synthesises the frameworks of Simon Sinek, Matthew Syed, and James Clear into a unified system for achieving high-stakes goals. Try the Goals Stress Test to check out your commitment to achievement

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

June 3, 2026

Employer Pension Contributions for Company Directors:

For a UK company director, a pension isn't just a retirement pot—it’s arguably the most powerful tax-planning tool left in the arsenal. Find out how you and your company can benefit.

Read MoreHealth & Fitness

Health & Fitness

Health & Fitness

June 3, 2026

Mental Fitness & Cognitive Reserve

Why more people are treating the brain like a muscle — and training for the long game

Read MoreTravel & Adventure

Travel & Adventure

Travel & Adventure

June 3, 2026

Health & Fitness

Health & Fitness

Health & Fitness

June 3, 2026

Health & Fitness

Health & Fitness

Health & Fitness

June 3, 2026

Get Ready for the Slopes

.jpg)

Transform your ski experience with our "Ski-ready Guide," the

essential pre-habilitation program designed to build a

stronger, injury-resilient body for the slopes. Discover the

four pillars of ski fitness—strength, core stability, agility, and

endurance—along with a comprehensive six-week workout

plan that ensures you glide effortlessly from the first chair

to the last run. Don’t let injury sideline your adventure;

Prepare your body now and conquer the mountain with

confidence.

Read MoreLifestyle Planning

Lifestyle Planning

Lifestyle Planning

June 3, 2026

Retire To The Sun

An overview of the most attractive overseas retirement destinations for UK citizens, covering visas, property, healthcare, and tax considerations. Explores the lifestyle appeal of sunbelt living alongside the practical realities of post-Brexit relocation planning.

Read More

Pensions & Finance

Pensions & Finance

Pensions & Finance

June 3, 2026

Managing Your Pension Fund Investment Profile

Your DC pension is a powerful investment tool for your future, but it needs your attention to reach its full potential.

By actively managing your pension, you're not just saving—you're investing in a more secure and prosperous retirement.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

June 3, 2026

The Retirement Illusion

Retirement should be designed — not drifted into.

“87% of UK adults have clear aspirations for retirement — but only 15% have a plan to afford them.”

– Barnett Waddingham, The At Retirement Reckoning (2025)

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

June 3, 2026

Risk Management in Retirement

Understand the key risks that can erode pension income over time and how to structure withdrawals to manage them.

Read MoreHealth & Fitness

Health & Fitness

Health & Fitness

June 3, 2026

Cholesterol: What You Need to Know

what we know—and what’s changing fast—about cholesterol, statins, and the future of cardiovascular prevention.

Read MoreHealth & Fitness

Health & Fitness

Health & Fitness

June 3, 2026

The Real Power of Walking

You don’t need fancy gear, a gym membership, or hours of free time. A pair of comfortable shoes and a commitment to move with intention are all it takes

Read MoreHealth & Fitness

Health & Fitness

Health & Fitness

June 3, 2026

We Don’t Age Gradually, We Age in Waves

Understanding when these bursts happen allows us to intervene early, at the times when lifestyle changes may have the biggest payoff.

Read MoreLifestyle Planning

Lifestyle Planning

Lifestyle Planning

June 3, 2026

Are You Retirement Ready?

True readiness goes beyond just money. This is a quick self-check—not a test, but a chance to reflect on how prepared you are for the next exciting phase of life.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

June 3, 2026

Is the UK State Pension Really That Generous? What the International Data Actually Shows

The triple lock debate rages on — but how does the UK State Pension actually stack up against our European neighbours? The data from the House of Commons Library might surprise you.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

June 3, 2026

MPs Call for Overhaul of Lifetime ISA (LISA)

A major parliamentary report has called into question whether the Lifetime ISA (LISA) is truly fit for purpose

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

June 3, 2026

IHT Latest Thinking

The winds of change are blowing through the UK's fiscal landscape, and a long-standing feature of estate planning – the inheritance tax gifting allowance – may be about to be swept up in the storm.

Read MorePensions & Finance

Pensions & Finance

Pensions & Finance

June 3, 2026

IHT Changes Explainer

From 6 April 2027, reforms will bring all pensions into the estate for IHT purposes. This guide sets out what’s changing, who is affected, and the strategies you can use to adapt.

Read MorePension Planning Knowledge Base

%20copy.jpg)

Select a Chapter to Read More

Contact information

Get In Touch

We're here to help you plan your retirement with confidence

______________

______________

FAQ's

Answers to some commonly raised questions

Is RetirePlan free to use?

Yes, our core planning tools are free. As the service develops we will also offer a premium tier with advanced features but we would expect early adopters to get the upgrade for free. That may exclude certain items such as face to face meetings, and of course any regulated advice.

Do you provide financial advice?

No, RetirePlan is a planning and educational tool, not a financial advisory service. We provide guidance information and calculators to help you make your own informed decisions. We strongly recommend consulting a regulated adviser when considering important financial decisions.

|Is my data secure?

Absolutely. We use data encryption and never store sensitive credentials.

Can I use RetirePlan if I'm already retired?

Absolutely! RetirePlan helps you manage your retirement income, plan spending, and track your finances in retirement.

Do you work with financial advisors?

We're exploring partnerships with independent financial advisors. If you're an advisor interested in working with RetirePlan, please contact us.

Can RetirePlan help with pension transfers?

We provide information to help you understand your options, but pension transfers require regulated financial advice. We can help you understand the questions to ask an advisor.

Yes, our core planning tools are free. As the service develops we will also offer a premium tier with advanced features but we would expect early adopters to get the upgrade for free. That may exclude certain items such as face to face meetings, and of course any regulated advice.

Do you provide financial advice?

No, RetirePlan is a planning and educational tool, not a financial advisory service. We provide guidance information and calculators to help you make your own informed decisions. We strongly recommend consulting a regulated adviser when considering important financial decisions.

|Is my data secure?

Absolutely. We use data encryption and never store sensitive credentials.

Can I use RetirePlan if I'm already retired?

Absolutely! RetirePlan helps you manage your retirement income, plan spending, and track your finances in retirement.

Do you work with financial advisors?

We're exploring partnerships with independent financial advisors. If you're an advisor interested in working with RetirePlan, please contact us.

Can RetirePlan help with pension transfers?

We provide information to help you understand your options, but pension transfers require regulated financial advice. We can help you understand the questions to ask an advisor.