The Triple Lock: Generous Policy or Political Football?

Few topics generate more heat in UK policy circles than the triple lock. Critics argue it's an unaffordable commitment to one generation at the expense of another. Defenders say it protects pensioners from poverty. But lost in the noise is a simpler question: generous compared to what?

A House of Commons Library research briefing published in October 2024 offers a rare, data-driven answer. And the picture it paints is more nuanced — and more sobering — than most of the debate acknowledges.

The Headline: The UK Sits Below the OECD Average

Start with the most striking finding. The UK's overall net pension replacement rate — that is, what you receive in retirement as a percentage of your pre-retirement earnings — is 54.4% from mandatory schemes. The OECD average is 61.4%. The EU27 average is higher still at 68.1%.

In plain English: a typical UK worker retiring today can expect to replace just over half their working income through mandatory pension provision. Their counterpart in France, Spain, Portugal, or the Netherlands will typically replace considerably more.

That doesn't feel like the story told by those who call the triple lock too generous.

Comparing State Pensions Directly: Where the UK Stands

The UK's New State Pension pays £221.20 per person per week in 2024/25 — a figure most working people would struggle to live on alone. How does it compare with broadly similar flat-rate systems elsewhere in Northern Europe?

- Ireland pays €277.30 per week (around £238) for a full contributory pension — around 8% more than the UK in cash terms.

- The Netherlands pays a single pensioner €361.28 per week (around £310) — 40% more than the UK equivalent.

- Denmark's Folkepension, once means-tested supplements are included, reaches £382 per week for a single pensioner — nearly 75% more than the UK rate.

There is a caveat worth noting: Denmark requires 40 qualifying years, Ireland 48, and the Netherlands 50 — all longer than the UK's 35. So the full rates aren't perfectly comparable. But even accounting for this, the gap is substantial.

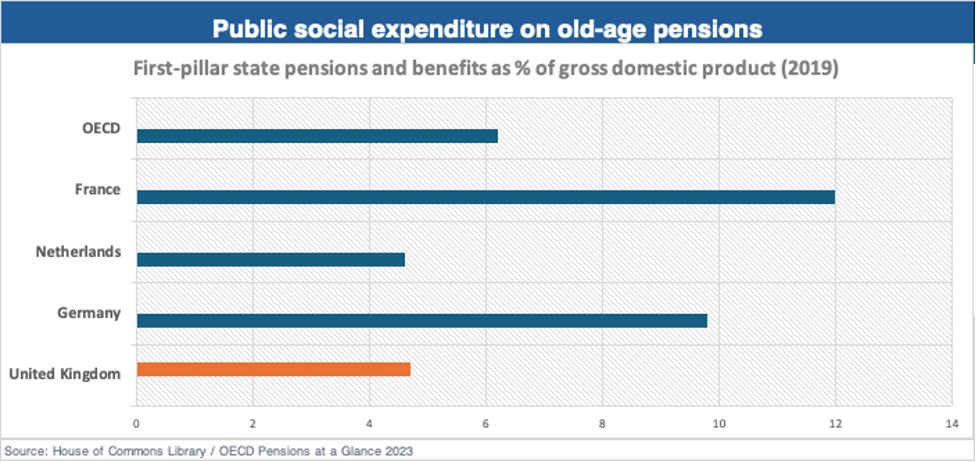

The UK also spends considerably less on state pension provision as a share of GDP. In 2019, the UK devoted 4.7% of GDP to first-pillar pensions and pensioner benefits — well below the OECD average of 7%, and a fraction of countries like Italy (12.8%), France (12%), or Portugal (12.4%).

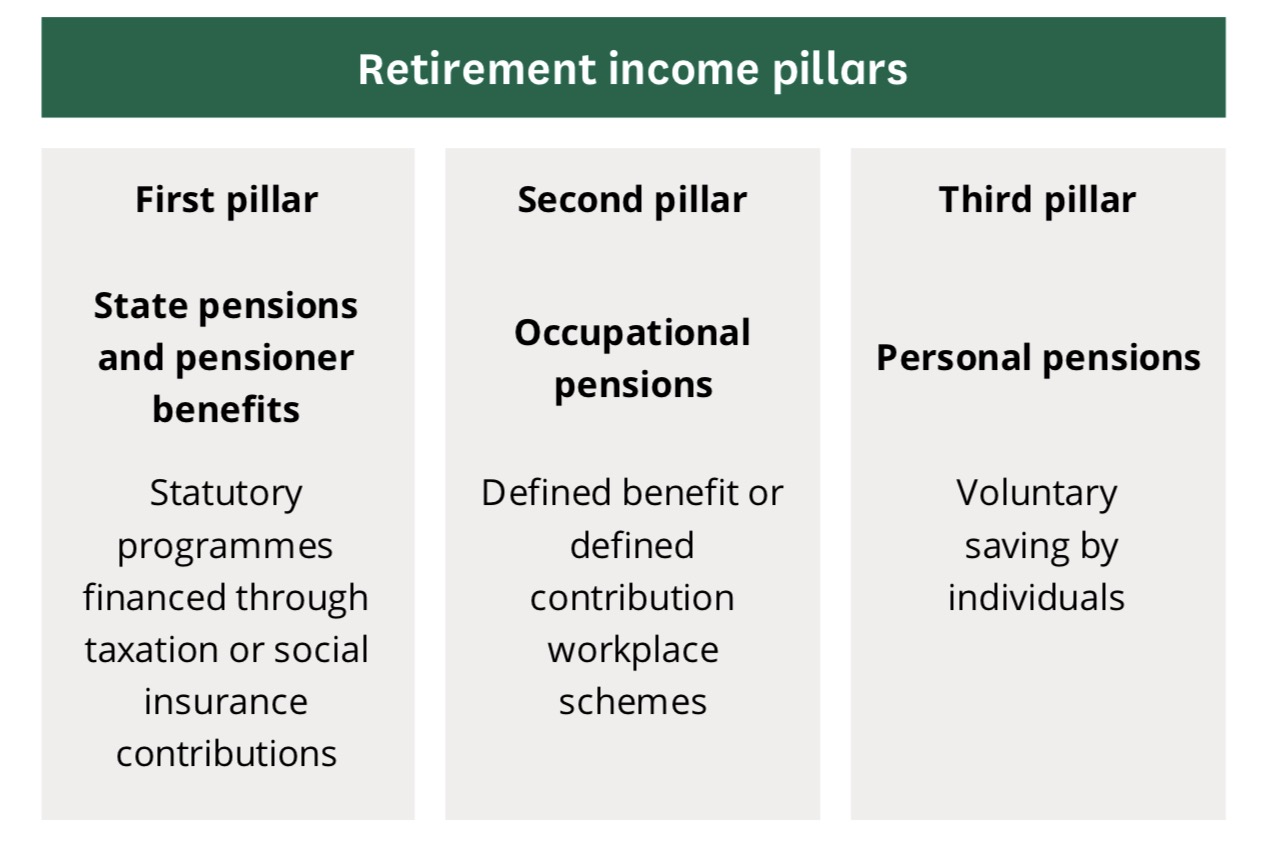

Understanding Why the Gap Exists: The Three-Pillar System

Most developed pension systems are built on three pillars. The first is the state pension — the baseline provided by government. The second is occupational pensions — workplace schemes, either defined benefit (final salary) or defined contribution. The third is personal savings — ISAs, SIPPs, and individual pension pots built up voluntarily.

Where countries differ is not just in the generosity of each pillar, but in how much they rely on each one. France, Germany, Italy, and Spain place enormous weight on the first pillar — their earnings-related state pensions are designed to replace a substantial proportion of working income on their own. The state does the heavy lifting, funded through high social insurance contributions from both employers and employees.

The UK made a different choice. Deliberately and over several decades, policy shifted more of the responsibility for retirement income from the state to the individual. The first pillar was kept relatively modest. The expectation was that occupational and personal pensions would fill the gap.

For much of the twentieth century, that worked reasonably well for those in stable employment with access to generous defined benefit schemes. But as DB schemes closed and the workforce became more fragmented — more self-employment, more part-time work, more career changes — the cracks widened. Many workers were simply not saving enough in pillars two and three to compensate for a lean pillar one.

The policy response was automatic enrolment, introduced in 2012. By making workplace pension saving the default rather than the opt-in, the government ensured that the majority of employed workers now have at least some second-pillar provision building up. Participation rates have risen dramatically as a result. But the minimum contribution levels — currently 8% of qualifying earnings combined between employer and employee — remain well below what most people will need for a comfortable income in later life. And the self-employed remain outside the system entirely.

So when the international data shows the UK's overall replacement rate at 54.4% against an OECD average of 61.4%, it reflects a system that was designed to rely on private saving to close the gap — but where that private saving has not always materialised at the scale required. The triple lock, in this context, is less a sign of generosity and more a recognition that the first pillar needed shoring up.

The Poverty Picture: Room for Concern

Perhaps the most uncomfortable data point in the briefing is on pensioner poverty. The OECD estimated that 14.5% of people aged 66 and over in the UK were living in relative income poverty in 2022 — defined as having incomes below 50% of the median. That placed the UK 14th highest out of 34 OECD countries for which comparable data was available.

Compare that with Denmark (4.1%), Norway (4.3%), France (5.8%), or the Netherlands (8.1%) — all countries with more generous state pension systems — and the direction of travel is clear. Lower state provision does not, in general, correlate with less poverty. It tends to correlate with more.

The UK's relatively high pensioner poverty rate is partly offset by the role of occupational and personal pensions. Around 39% of UK pensioner income comes from occupational pensions — a much higher proportion than in many continental European countries, where state provision is dominant. But that private income is unevenly distributed. Those who built careers with strong workplace pension schemes do well. Those who didn't, don't.

So Is the Triple Lock Too Generous?

The honest, data-led answer is: probably not — at least not by international standards. The triple lock exists precisely because the UK State Pension started from a low base and needed a structural mechanism to close the gap with comparable countries. Whether it's the right long-term mechanism is a legitimate policy debate. Whether the pension itself is lavish, by any objective international measure, is not.

For anyone planning their own income in later life, the implication is clear: the State Pension alone — even with the triple lock — is unlikely to be enough. Building additional private savings through workplace pensions, ISAs, and personal pension contributions remains essential. It's not a luxury. It's the foundation of financial independence in your next chapter.